Saving for a house deposit

Many Australians consider saving for a house deposit as one of their biggest financial challenges. See how it can be made easier.

Many Australians consider saving for a house deposit as one of their biggest financial challenges. See how it can be made easier.

Depending on where you'd like to buy, the house deposit amount you'll need is going to be different.

Generally, you need 20% of the home purchase price for a house deposit, but in some instances, your deposit could be as little as 5% if you can pay for Lender's Mortgage Insurance.

The average price of residential property in New South Wales is $871,800, which means an average

deposit could be $174,200. In Victoria, the average house price is $736,800 which equates to an average deposit of $147,2000 (as of June 2020 from the ABS). Your loan-to-valuation ratio will also determine how much you need for your home deposit.

Since saving for a house deposit in Australia can cause massive financial pressure, we've compared the most popular strategies to help you reach your goals and buy your dream home.

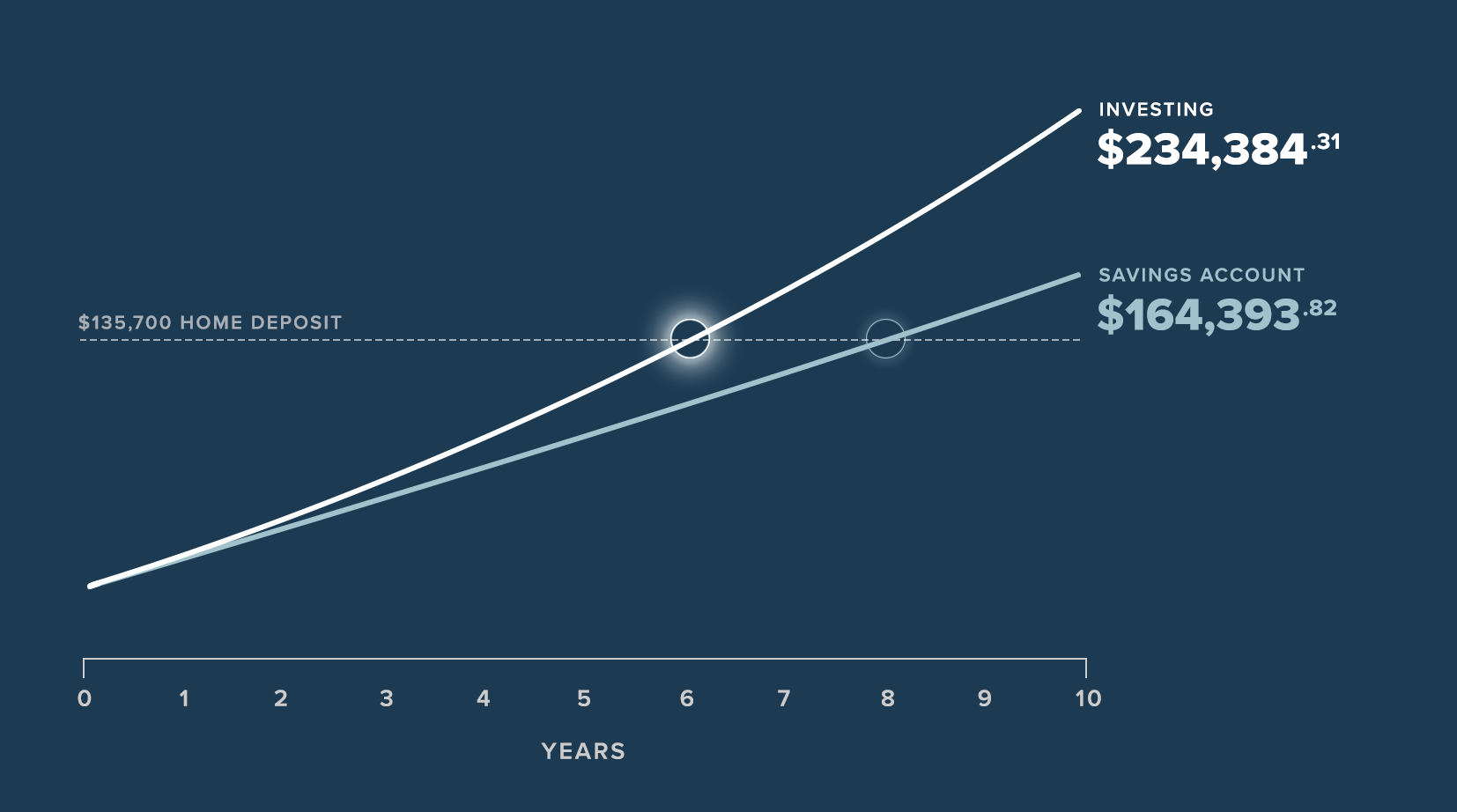

Average house deposit: $135,700

Average house deposit: $135,700

As of June 2020 (Source: ABS)

High-interest savings or term deposits

Historically, both of these options have been a popular, reliable way of maximising your savings.

However, with the current low interest rate environment, the growth of your initial investment will be slow.

Low growth

Available to anyone

Low risk

Using superannuation contributions

The First Home Super Saver Scheme (FHSS) only applies to first home buyers.

It allows eligible buyers to withdraw the voluntary super contributions for use towards a home deposit.

Super contributions can be made through salary sacrificing or through after-tax contributions.

Potential for high growth

First home buyers only

Lower risk than DIY investing

DIY investing

Investing can be an alternative to saving, and often a much faster way of growing your money over a period of time (generally more than 3 years).

If you're investing to save for a house deposit, you should avoid stock-picking and stick to a strategy that suits your comfort with risk.

Potential for high growth

Available to anyone

High risk

Automated investing

Another way to grow your money is to invest in a diversified portfolio that's managed by a low-fee investment advisor.

With regular top-ups, your money can grow steadily and with little effort, as it's invested by human experts and rebalanced when markets change. See how it works.

Potential for high growth

Available to anyone

Lower risk than DIY investing

With interest rates at an all-time low, investing may be a good option for you to grow your savings faster.

$10,000 invested in a broad mix of investments earning 7% per annum could reach a deposit goal of $135,700 2 years earlier than if it was kept in a savings account.

Start investing

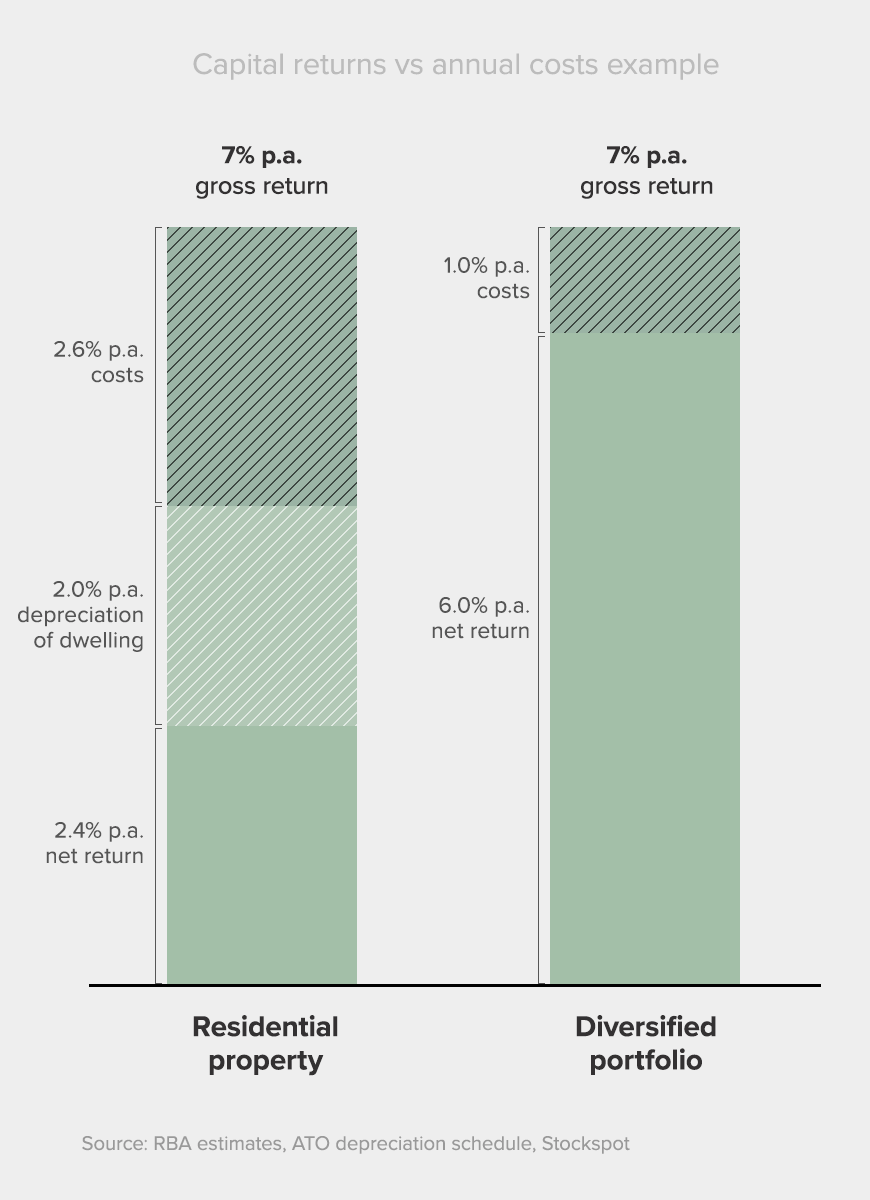

Many Australians think property investing is the only option for long term wealth growth, but property investing returns may be lower than you think.

As of October 2020, the gross yield (rent) on houses in Australia is 2.8%, and 3.8% for apartments (SQM Research). This doesn't take into account the substantial running costs, council rates, management fees, property maintenance and repairs/renovation. Find out more about investment property returns before you make a decision.

It's worth looking in to alternatives to property investment like a diversified ETF portfolio.